- Opinion

- No Comment

Trust, Gold, and Commitment: Rethinking Zimbabwe’s Monetary Future

By Craig J. Richardson

Since the year 2000, Zimbabwe’s residents and investors have seen savings and investment destroyed by hyperinflation—a product of monetary policy that prints money to cover enormous budget deficits. In other countries, traditional remedies like using a stable foreign currency or a currency board often work, but in Zimbabwe’s case, the government’s disregard for the restrictions only perpetuates the inflation cycle. This article proposes a novel solution for the government to regain social trust: place a substantial amount of Zimbabwe’s reserves in a Swiss-law-governed trust with automatic enforcement mechanisms, which could lead to stable GDP growth and inflation rates.

Introduction

Over the past 25 years, Zimbabwe’s residents and investors have been whipsawed by inflation, destroying their savings and killing the incentive to work and invest. Between 2006 and 2024, six new currencies have been introduced. None of them has ever been accepted as payment outside of the country’s borders.

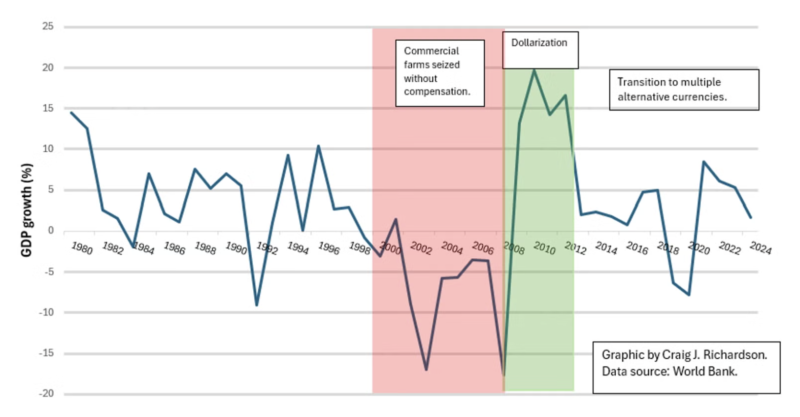

The crux of the problem has been the monetary policies of the Reserve Bank of Zimbabwe (RBZ), which, unlike the Federal Reserve of the United States, has little independence from the spending excesses of Zimbabwe’s national government. Over the past 25 years, Zimbabwe’s two Presidents have explicitly controlled the RBZ, ranging from domestic bond purchases to foreign currency borrowing. The RBZ has established a clear pattern of monetary abuse since the year 2000: 1) Excessive government spending is financed by printing money in the current currency; 2) runaway inflation takes hold; 3) a stable foreign currency is forcefully adopted to prevent economic meltdown; 4) a relatively stable period of prices is achieved; 5) a new Zimbabwe currency is introduced with great fanfare; 6) the cycle starts again. The result has been an unsettling rollercoaster ride for the country’s GDP since 2000, as seen in Figure 1.

For many Zimbabweans whose lives have been shattered by these broken monetary commitments, leaving the country was the only choice. Since 2000, according to estimates by the World Bank, roughly half of Zimbabwe’s professionals have fled the country. A new “out-of-the-box” policy is needed, one that breaks this pattern of monetary irresponsibility and is grounded in verification, transparency, and accountability. A stable currency is fundamental to rebuilding a country rich in minerals, wildlife, and geographical wonders. Trust in stable money is the bulwark of any well-functioning economy.

Broken Trust: Origins and Continuity

The erosion of institutional trust can be traced to the land reform movement in the early 2000s. Prior to 2000, Zimbabwe had experienced relatively stable growth, low inflation, and was known as the “jewel” of Africa. Rich in raw materials and productive farmland, it grew enough food to feed its people and export the rest.

The political underpinning of these land reforms was a clear divide in wealth: 4,500 white families owned most of the commercial farms. In contrast, 840,000 Black farmers subsisted on communal lands—a legacy of colonialism. In 2000, everything changed. Thousands of white-owned commercial farms were seized by the Mugabe-led government, undermining property rights that had been protected under a Western-inspired constitutional framework.

The so-called solution addressed the wrong problem. Black farmers lacked title deeds and access to credit for investing in their farms. Rather than expanding property rights, Mugabe invalidated farmland titles to expedite redistribution. While this redistributed wealth in the short term, it neglected to recognize the largest invisible asset: the expertise to run a complex farming enterprise. That knowledge vanished as commercial farmers fled abroad.

In the wake of the land reforms, the disastrous ripple effects continued. Falling agricultural productivity and production created widespread food shortages, leading Zimbabwe to develop a dependence on organizations like the World Food Program in order to feed itself. The broken trust in the government of Zimbabwe was illustrated by a sharp 99 percent drop in foreign direct investment and a jump from 3.4 percent in 2000 to 20.4 percent in 2001 for the risk premium on investment.

All of this set the stage for the second-worst hyperinflation any country has ever experienced. As tax revenue plummeted due to the collapsing economy, the government had two choices: drastically cut spending or print money. It unfortunately chose the latter to cover skyrocketing deficits. By the end of 2003, inflation had passed 500 percent per year. And still, each year, the deficits grew larger, and so did the money supply, fueling an exponential rise in prices. At its height in November 2008, inflation snowballed to almost 80 billion percent per month. Stories abound of how Zimbabweans adapted to extreme hyperinflation. One trader requested a swap of beans for fuel rather than accept worthless Zimbabwe dollars. A local merchant who imported wine needed to open a second business in England to pay for the wine in an acceptable currency. Indeed, almost all businessmen were and still are required to spend a great deal of time deriving ingenious schemes to avoid the use of Zimbabwe’s junk currency.

The Promise and Failure of Dollarization and the Gold-Backed ZiG.

By late 2008, 100 trillion Zimbabwe dollar notes were worth 40 cents, and the government’s back was against the wall. It eventually decided to “dollarize” in 2009. The dramatic yet popular move prompted the economy to rebound with great strength. Without the ability to print U.S. dollars, inflation stabilized. However, by the summer of 2018, the Zimbabwe government was employing creative workarounds to evade the fiscal constraints of dollarization. To “solve” government deficits caused by foreign exchange shortages, the RBZ issued special Zimbabwe bonds and advertised them as dollar-denominated promissory notes that banks could not actually redeem. On the street, these bonds traded at roughly 60 cents on the dollar.

Met with little success, in 2019, Zimbabwe abandoned dollarization and resumed printing its own currency. Predictably, it depreciated rapidly. By early April 2024, the Zimbabwe dollar traded at roughly 40,000 to 1 U.S. dollar on the unregulated market.

Never one to run out of new ideas, Zimbabwe introduced the Zimbabwe Gold (ZiG), supposedly backed by $285 million of hard assets, including gold and foreign currency. The official rate was 2.50 ZiG per U.S. dollar. In an effort to shore up trust in the currency, there was even a “surprise” presidential inspection of gold reserves, as if to prove the gold had not yet been stolen.

Yet six months later, the deep mistrust of the government—shaped by the memory of commercial farm and diamond mine seizures—undermined the ZiG as it lost half its value on unregulated markets. While inflation is far better than in the past, the currency is barely circulated throughout the country and not accepted outside its borders, indicating a continuing crisis of trust in any Zimbabwean currency.

Policy Recommendations: Externalized Enforcement Using a Trust to Build Trust

Since the underlying issue is that of trust, Zimbabwe can convey the seriousness of its intent to stabilize the money supply by agreeing to an international oversight mechanism. If Zimbabwe voluntarily turned to Switzerland—a country with a storied history since the 18th century as a geopolitical “safe haven,” along with a stable currency, banking system, and strong regulatory oversight—this would be an ideal international signal that the country is serious about monetary reform.

A Swiss-law-governed independent trust with substantial holdings of Zimbabwean gold and stable, low-interest foreign bonds could be the solution. The trust would not rely on political discretion, but on enforceable Swiss contract law that would contain automatic financial triggers if inflation targets are breached. It would also include a reward system for RBZ’s responsible management of monetary policy.

The goal is not forfeiture of assets, but credible proportional penalties that keep Zimbabwean monetary policy on track as well as send a continuous and credible signal to international markets. There are two pillars to this arrangement that provide incentives for stable monetary policy. The first pillar would hinge on independent monitoring and transparency. Reserve holdings would be independently held and audited by a well-regarded Swiss firm and publicly reported at regular intervals, with transparent balance sheets. Transparency alone lowers risk premiums and signals earnestness. An excellent candidate would be KPMG Switzerland, which already has extensive experience auditing central banks and sovereign entities, and could partner with a Swiss custodian bank, such as UBS, to hold the gold and other assets.

The “teeth” of this proposal—its second pillar—lie in accountability with contractual rules built into the trust. For example, if the 12-month inflation rate exceeds an agreed five percent ceiling for a sustained period, a predetermined share of reserve earnings would automatically be diverted into a stabilization account held under Swiss jurisdiction. The earnings would then be inaccessible until compliance is restored. This imposes a measurable fiscal cost without a destabilizing forfeiture of the country’s assets.

Critics may argue that such rules “handcuff” the government during crises such as droughts. Yet, if policymakers know they cannot rely on monetary expansion as an escape valve, they will diversify the economy, build fiscal buffers, and strengthen property rights before crises occur. Furthermore, it signals to Zimbabweans and investors alike that monetary discipline is no longer optional, making the country financially attractive once again.

Conclusion

Since seizing commercial farms in the early 2000s and substantially weakening property rights, Zimbabwe has had a continuous reliance on printing money to bypass fiscal and monetary discipline. Runaway inflation over the past 25 years has substantially eroded trust in the Zimbabwe government, along with the incentive to work, save, and invest.

Perhaps the best—and only—way forward in repairing faith in the country’s monetary system is to create an independent trust governed and audited by Swiss law, with substantial holdings of Zimbabwean gold and stable, low-interest foreign bonds held by a Swiss bank. Built into the Swiss trust would be a reward and punishment system for both the government and the Reserve Bank of Zimbabwe, based on their success in achieving monetary stability. If voluntarily chosen by the government, this policy would signal seriousness to internal and international stakeholders, creating a legitimate hope for Zimbabwe’s long-term success in creating a durable and successful currency and economy.

. . .

Craig J. Richardson is the Truist Distinguished Professor of Economics at Winston-Salem State University and the author of The Collapse of Zimbabwe in the Wake of the 2000-2004 Land Reforms (Mellen Press, 2004) as well as numerous articles about the country. His work focuses on economic networks and property rights and how they link to economic development. He currently serves as the founding director of the nationally recognized Center for the Study of Economic Mobility at his university.