- Opinion

- No Comment

The new Zimbabwean ZiG: Sixth time a charm?

Zimbabwe’s historical relationship with money has been inundated with mistakes, recklessness, and hardship. During the peak of its 2008 hyperinflation, the nation experienced a catastrophic economic downturn, characterized by the issuance of billion- and trillion-dollar banknotes that were, despite their nominal enormity, virtually worthless.

Recent economic challenges have revived painful memories of that era with the resurgence of inflation (currently at 55 percent), a return to the US dollar, euro, and South African Rand as de facto currencies, and the necessity of using large physical stacks of bills to purchase basic commodities like bread and eggs.

On April 5, a new currency was announced. Later this month, the ZiG (Zimbabwe Gold) will replace the current monetary unit, the Zimbabwean Real Time Gross Settlement dollar (RTGS). The ZiG marks a sixth attempt by the Zimbabwean government and central bank to introduce a currency unit that sets its monetary house in order.

Upon declaring independence in 1980, the Reserve Bank of Zimbabwe (RBZ) issued the original Zimbabwe dollar (ZWD) to replace the Rhodesian dollar at par (1:1). Over the subsequent two decades, the money supply expanded amid fiscal mismanagement, policy errors, and authoritarian governance.

Denominations of the ZWD grew from two, five, and 10 ZWD denominations into bills marking hundreds, thousands, and millions of units, each with precipitously dissipating purchasing power.

In August 2006, the first attempt to reform the original ZWD was undertaken. The RBZ recalled outstanding currency notes, replacing them with redenominated notes of one one-thousandth the value of the previous notes by slashing three decimal places.

Roughly two years later, in August 2008, a second redenomination marked the third ZWD reissue, this time slashing ten decimal places. By this point, prices were at least doubling on a daily basis. Thus did each ten billion ZWD note become one ZWD to address the increasingly unwieldy terms of face-to-face market transactions.

The apex of the hyperinflation was reached with the issue of the 100 trillion ZWD banknote, after which in February 2009 — barely six months later the previous redenomination — twelve zeros had to be removed from currency units. This was the fourth ZWD issue.

By this point, the 1980 ZWD had been whittled down to one-sextillionth (0.000000000000000000001) of its initial value. Errors in simple transactions became commonplace, with both calculators and computers unable to handle fundamental accounting operations. Agriculture, a difficult commercial undertaking even with a stable currency, is all the more challenging when consummated in units usually reserved for astronomers.

By the end of 2008, 28 years of inflation topped a total 231 million percent. The ZWD was demonetized in 2009, with the Euro, the South African Rand, and the US dollar as well as smaller, regional currencies supplanting it. In 2015, that process was completed, with every 35 quadrillion ZWD presented at a bank being retired for a single US dollar. Alongside a wide array of currencies in use throughout the next few years were Zimbabwean government bond notes.

In 2019, the Real Time Gross Settlement (RTGS) dollar was issued, but quickly ran into trouble — even before the COVID pandemic broke out. Inflation followed yet again, and the use of international currencies — which had been outlawed upon the introduction of the RTGS — was again legalized.

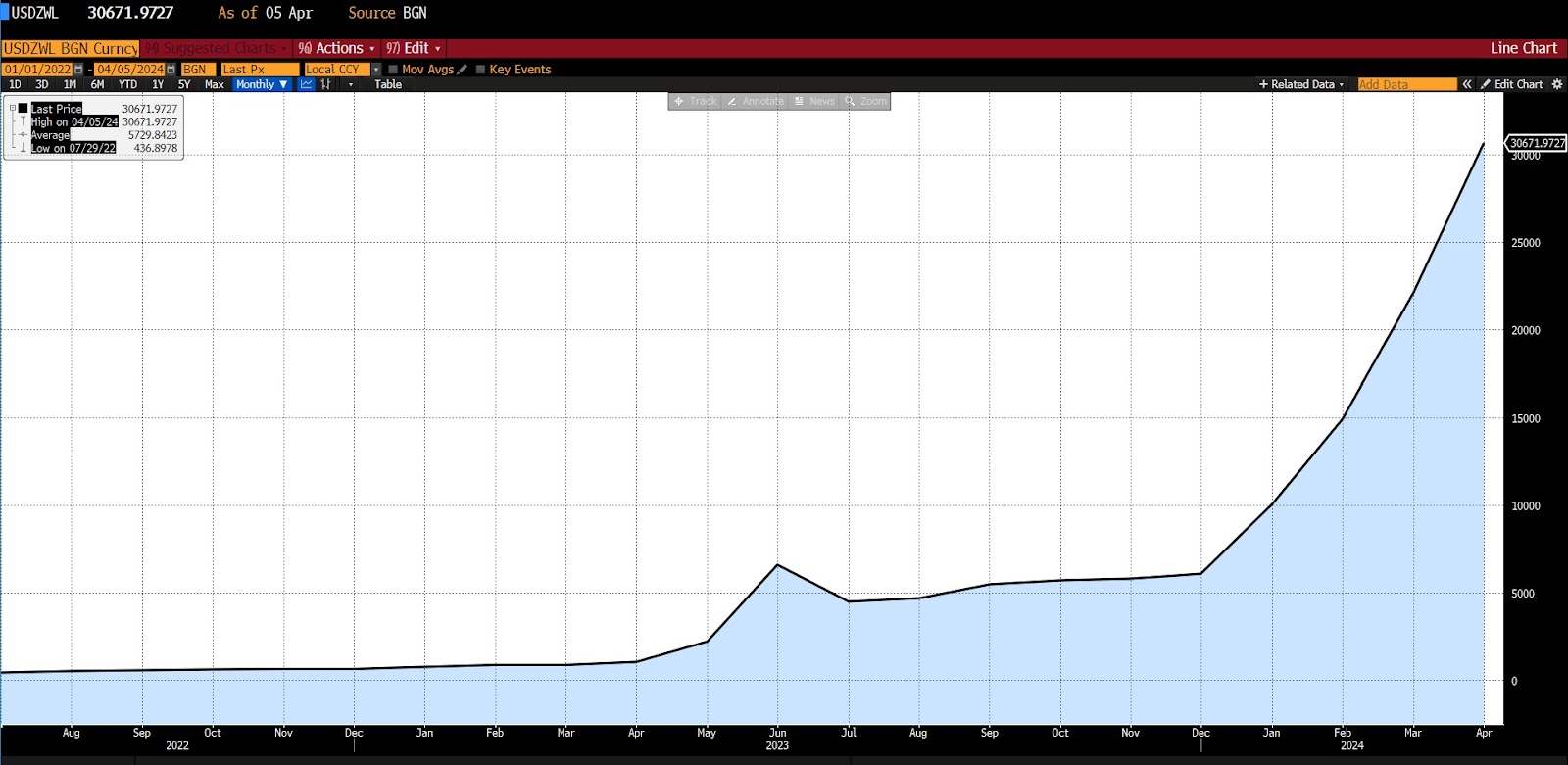

When issued, the RTGS was set at an official exchange rate of 2.5 per US dollar. Since the start of 2024, though, it has lost 80 percent of its value, recently trading at 30,671 per US dollar. At this rate of inflation, an item that cost $100 US dollars in 1980 would have cost over $700 billion dollars by 2023.

USD-ZIM/RTGS exchange rate (2022 – present)

On April 30, 2024, RTGS units will be exchangeable for ZiG as the new coins and bills begin circulating. RBZ Governor John Mushayavanhu has announced the initial exchange rate for the ZiG at 13.56 per US dollar, with subsequent rates to be determined through interbank markets.

Hopes for the success of the ZiG are underpinned by a reputed $185 million worth of gold and other reserves backing it. There are practical hurdles, though. The sustainability of a gold-backed currency like ZiG is uncertain considering the limited extent of Zimbabwe’s physical gold reserves relative to the desired exchange rate.

Moreover, the absence of concurrent measures from its trading partners leaves the new currency susceptible to fluctuations in gold prices. Black markets, which speak truth to a fault, are registering doubt.

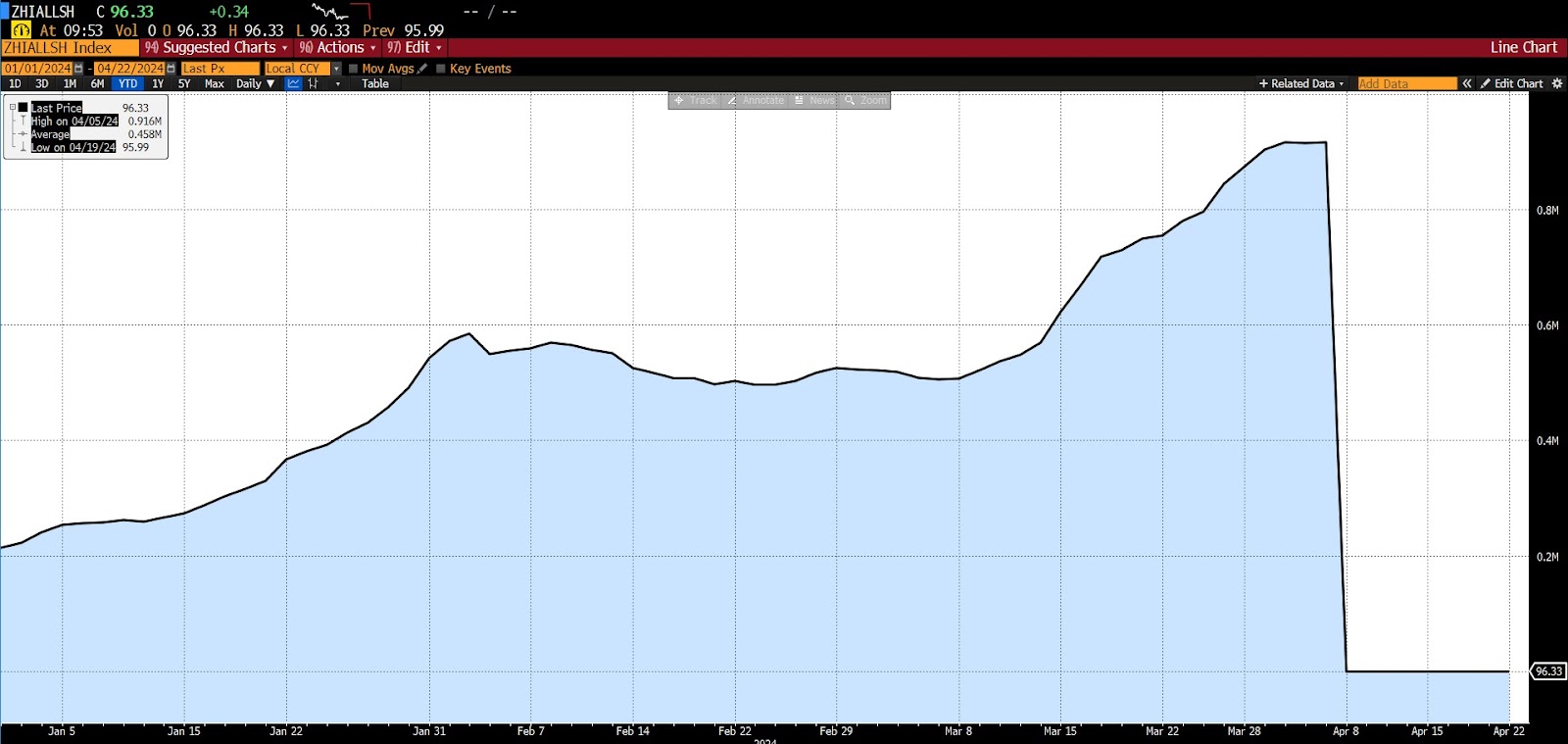

And investors in the Zimbabwe Stock Exchange in Harare have made no secret whatsoever about their cynicism, sending stock prices down 99 percent in several hours after the ZiG announcement.

Zimbabwe Stock Exchange (Jan 2024 – present)

Zimbabwe still relies upon printing money to finance its budget deficits. Although Mushayavanhu has adamantly pledged to avoid this practice, at the onset the ZiG faces an uphill battle to claim public trust, given nearly a half century of monetary disasters.

Moreover, the government’s insistence on accepting payments for certain services exclusively in US dollars, such as road toll fees and passport processing, is undermining confidence in the new money even before it begins changing hands. Reports indicating that the government will require tax payments in mixed currency are further dimming prospects for the ZiG’s acceptance and viability.

The Zimbabwean government has, in addition, associated the latest monetary project with the global dedollarization movement. While there remains a possibility for the ZiG to outperform its predecessors, the country’s tumultuous economic history, transitioning from hyperinflation to hyper-dollarization and currently grappling with double-digit inflation and interest rates, underscores deep-rooted issues beyond mere monetary policy, including governance deficiencies and corruption risks.

Ruinous policies which have destroyed the productiveness of the nation’s economy, as well as the classic blame-mongering of businesses for the rising general price level (something Americans have borne witness to recently as well) have been commonplace.

Without comprehensive fundamental reforms addressing these systemic challenges, Zimbabwe risks perpetuating its reliance on emigration as a coping mechanism alongside the enduring symbol of its economic turmoil, the multi trillion-dollar banknote. The efficacy of any monetary system, whether a commodity standard or any other, hinges singularly upon the integrity and competence of its custodians.

Dissipated Zimbabwean cash is thumbtacked to many a bulletin board, and fetches many more US dollars in exchange on eBay than it ever did in its circulatory prime. The trinketization of that money, however, has come at great human cost.

According to the US Agency for International Development, a staggering 63 percent of Zimbabwean households endure poverty, with one in eight experiencing extreme deprivation. T

hat juxtaposes with the nation’s abundant mineral resources, spanning over 40 distinct minerals: platinum group metals, gold, coal, lithium, and diamonds among others. Despite that potential wealth, the realization of economic advancement remains contingent upon substantive political reforms.

Even the most faithfully implemented commodity-backed money standard is fundamentally predicated on the integrity and competence of its overseers. Successive waves of spectacular currency destruction speak to a deeper illness in economic and political institutions, strongly alluding to systemic vulnerabilities.

One hopes, for the sake of the long-suffering citizens of Zimbabwe, that this time around the result of yet another monetary reconstitution is successful, fostering a stable general price level, a reliable monetary unit for saving and spending, and enhanced possibilities for economic calculation.

Without fundamental changes guaranteeing private property protection, pro-market reforms, and safeguards against corruption, though, the ZiG is likely to retrace the unfortunate steps of its predecessors.